Warning Flags For Home Construction

[ad_1]

Vertigo3d/E+ via Getty Photos

By Robert Hughes

Full housing starts off fell to a 1.724 million yearly fee in April from a 1.728 million tempo in March, a .2 p.c minimize. From a year ago, whole starts off are up 14.6 %. Overall housing permits also fell in April, submitting a 3.2 percent drop to 1.819 million vs . 1.879 million in March. Whole permits are up 3.1 % from the April 2021 amount.

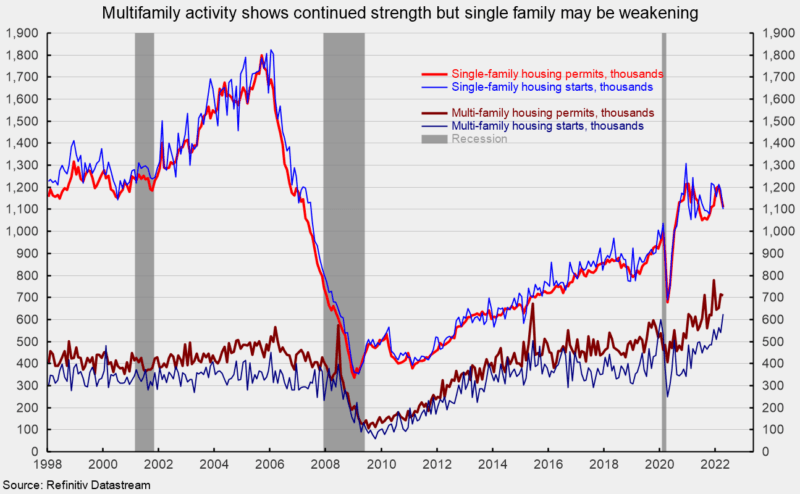

Commences in the dominant one-household section posted a fee of 1.100 million in April vs . 1.187 million in March, a drop of 7.3 per cent but are even now up 3.7 per cent from a calendar year back (see to start with chart). One-family permits fell 4.6 per cent to 1.110 million as opposed to 1.163 million in March (see very first chart).

Starts off of multifamily constructions with 5 or much more models amplified 16.8 per cent to 612,000 and are up 42.3 % around the earlier year when starts off for the two- to 4-loved ones-unit phase fell 29.4 % to a 12,000-device speed vs . 17,000 in March. Mixed, multifamily begins ended up up 15.3 percent to 624,000 in April and clearly show a achieve of 40.5 per cent from a 12 months in the past (see initial chart).

Multifamily permits for the 5-or-extra team fell .6 per cent to 656,000 whilst permits for the two-to-four-device category lowered 5.4 percent to 53,000. Blended, multifamily permits were 709,000, off 1. p.c for the month but up 15.7 percent from a yr ago (see very first chart).

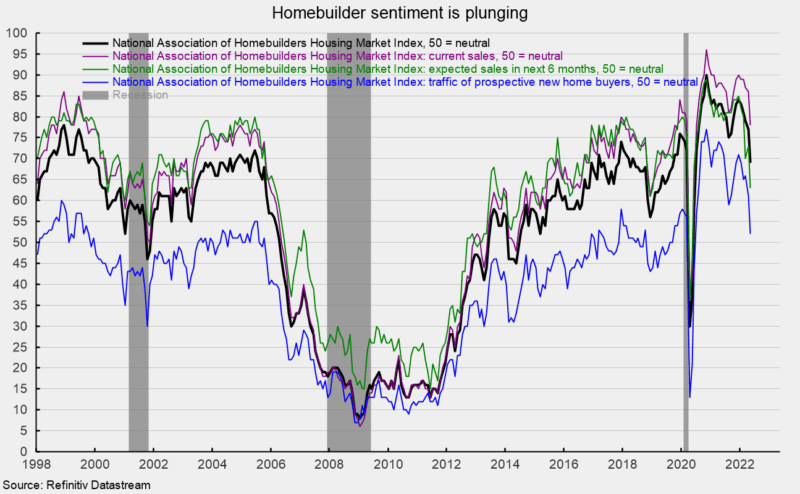

In the meantime, the Countrywide Association of Residence Builders’ Housing Marketplace Index, a evaluate of homebuilder sentiment, fell yet again in April, coming in at 69 as opposed to 79 in April, and down sharply from current highs of 84 in December 2021 and 90 in November 2020. Mounting mortgage loan prices, elevated home prices, and better input expenses are significant issues (see next chart).

All 3 components of the Housing Sector Index fell sharply in April. The expected solitary-family members sales index dropped to 63 from 73 in the prior thirty day period, the present solitary-household profits index was down to 78 from 86 in April, and the visitors of prospective purchasers index fell to 52 from 61 in the prior thirty day period (see next chart).

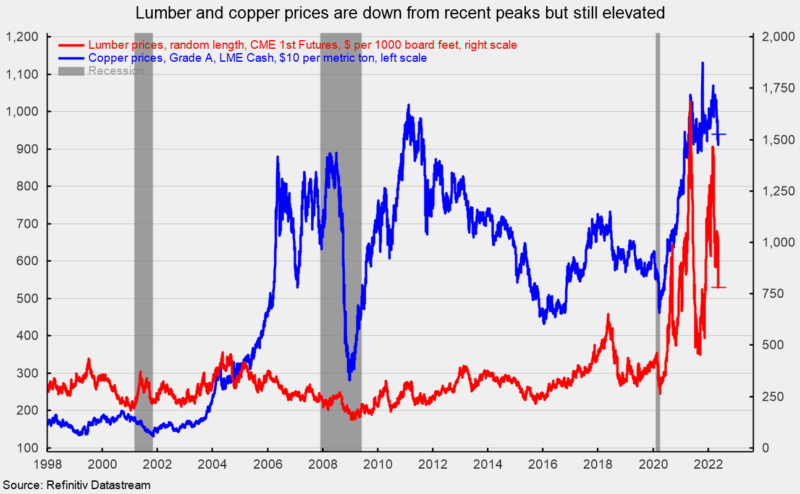

Enter expenditures are a problem for builders. Essential enter resources prices are down from peaks but continue to elevated with lumber coming in at about $780 for every 1,000 board toes in mid-May, down from peaks all-around $1,700 in Might 2021 and $1,500 in early March 2022 whilst copper was down marginally at $9,400 for each metric ton (see 3rd chart). The substantial enter charges will tension income at builders and may guide to additional rate raises for new residences (see fourth chart).

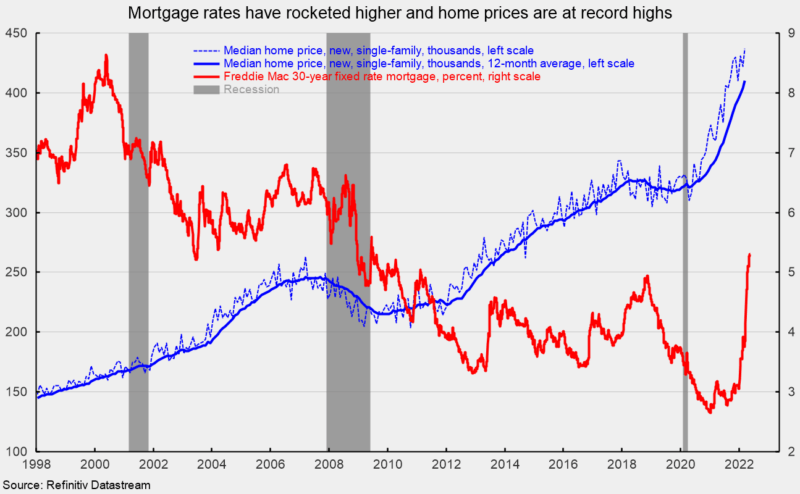

In addition, home loan premiums have rocketed higher a short while ago, with the level on a 30-year fastened charge house loan coming in at 5.30 per cent in mid-Could, just about double the lows in early 2021 though house prices are at record-substantial levels (see fourth chart). Bigger house prices and increased mortgage loan charges are most likely to be significant headwinds for upcoming housing action.

While the implementation of lasting distant working preparations for some workers might be delivering ongoing assistance for housing demand, file-substantial residence charges blended with the surge in house loan rates will most likely do the job to great exercise in coming months. Threats to long run demand put together with elevated input costs are sending homebuilder sentiment plunging. The outlook for housing, specifically the one-household phase, is deteriorating swiftly.

Editor’s Observe: The summary bullets for this short article ended up chosen by Seeking Alpha editors.

[ad_2]

Source website link